The goal for many in 2013? BUY A HOUSE

Due to the housing prices beginning their rebound and interest rates still at a very low percent how can you question yourself having this goal? This argument of Rent Vs. Buy has been around for decades and will stay around for decades.

Realistically, you should. It is a right choice for some in their finances and possibly wrong for others.

Most times it is going to depend on where you live, how much you have saved and what your plans are for the future.

After much debate here is what I recommend considering when you are determining which will have the bigger benefit for you, renting vs. buying.

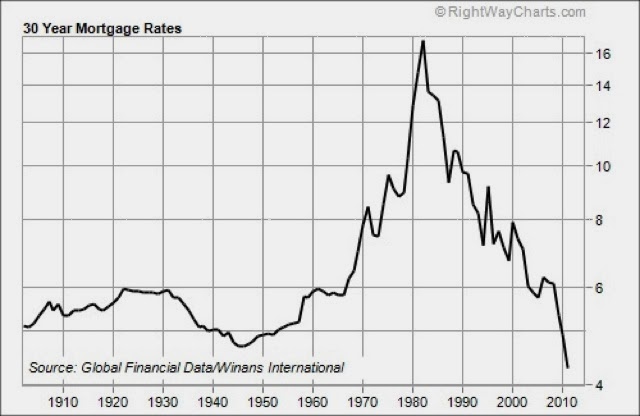

1. Market Trends

Have you ever heard the saying “location, location, location”? This saying will hold true now and forever but to that we could add: “timing, timing,

timing.”

Anyone whom may have watched the rise and fall of the housing market in the past 10 years can be a spokesperson for this addition of “timing” and how it has a lot to do with deciding whether purchasing ends as a good investment or dead weight in your finance portfolio.

This year alone I have seen many houses sell at half the price they were in years past, which just goes to show you that home values can, and do increase and decrease in value. Basically the only thing you want to take away from this paragraph is to AVOID purchasing a home at the peak of the market. Duh, you already knew that.

The harder thing to think about is how to avoid not buying at the peak of the market. To help easily answer this question I have found this great chart that gives you the answers. Simply follow the link and enter the data you are looking at in renting vs. owning. The graph will spell out what years renting would be best and which buying would be best. It will also point out your savings over time.

Buy Vs. Rent Calculator

2. Your Financial Picture

One of the major considerations you have to make is this: does your

current financial picture put you in a strong position to own a home? If not, then buying a house will not be the answer no matter what the market trends in section 1 favored.

If you have not started the process of evaluating your finances to see if you are prepared to purchase a home you should sit down and take a serious look at your bank accounts as well as your income and potential future earnings. Also, job security.

Decide how much debt you are carrying and how long you are looking at paying it off. It may hurt at first, however without taking a serious hard look at it, it won’t clean itself up without a plan. If you are carrying a lot of debt and if

you’re struggling to make your payments, this may not be the time for you to buy. Home ownership is a very large commitment and no one wants to see you end up on the hook for a large loan you cannot afford. In addition, you may not be able to secure a good interest rate if your debt to income ratio is higher than normal.

Another major factor is your job security and history. Some things to avoid are ending up in a location that doesn’t have great job potential. Things you want to think about and avoid are will you end up burning thru your savings if you lose your job? Also what is the possibility of losing your home and the equity you have built? Think carefully about any potential threats to your job and career

before making the decision to purchase a home.

What are your savings?

If you aren’t scared off from home ownership yet the next factor you are looking at is how much savings you have. Most home purchases require 10 percent or 20 percent as a down payment

on your mortgage. Check with your lender to see if you qualify for any first time home buyer loans or other ways you may be able to lower your down payment to possibly 5 percent (or even 3 percent in some cases). Keep in mind that while this sounds good now it will increase your

monthly payment because it will mean your total loan amount will be

larger- choosing your battles.

Your right down payment and home loan amounts will depend

on the factors we have covered above. In general it’s better to have a lot

saved up before applying for your mortgage. If you have cash for 20 percent down,

you will feel more confident because you’re more likely to be

approved for the loan and your monthly mortgage payments will be

lower and more manageable.

Future Plans?

One thing you hear people talk about is that it doesn’t

make sense to buy a house if you plan to move in the next five years — which is absolutely great advice since its TRUE. Buying a house requires lots

of fees and transactional costs (escrow, title, insurances etc) — these costs are unavoidable and can

total up to 5 percent of the cost of the house or more.

What this means is that if you buy a house and then quickly sell it again you will have to pay both the buying and selling costs of the home purchase, and, in a short time period. In most cases you won’t live in the house

long enough to enjoy the financial benefits of home ownership as the market is most likely not to shift that dramatically in

appreciating in your home’s value.

All in all it still depends on your individual situation. A general

rule of thumb is to avoid buying if you expect you’ll need or want to move

anytime soon.